July 27, 2024, 3:04 a.m.

Should you still invest in retirement annuities?

July 17, 2023

6

2192

0

Author

FinseshA hot topic not scrutinized enough. Let's explore.

A hot topic in personal finance, not scrutinized enough. We will delve into this contentious topic, explore alternatives to invest your hard-earned money, to make informed decisions.

This article is for hard-working South Africans, who are saving for retirement and placing their trust in the government to ensure they retire comfortably. This article is for the average man and woman needing an honest view of retirement annuities to determine if you should still invest in retirement annuities.

Retirement Annuity fund alternative

In a previous article, I discussed retirement annuities, how they work, and some of the pros and cons. You can read about it here. We will start exploring retirement annuity fund sectors vs the MSCI World index as a proxy for global investments over the last decade ending 31 December 2022. The idea is to remove the patches of advertisements placed in front of our eyes and do our research to find out if it's worth investing in a retirement annuity fund.

There are many alternatives out there, such as business investing, or property investing. By investing your cash flow to be tied up in a product can restrict you from capitalising on alternative opportunities. Lets focus on offshore investing as an alternative for now.

Retirement annuity vs global investment

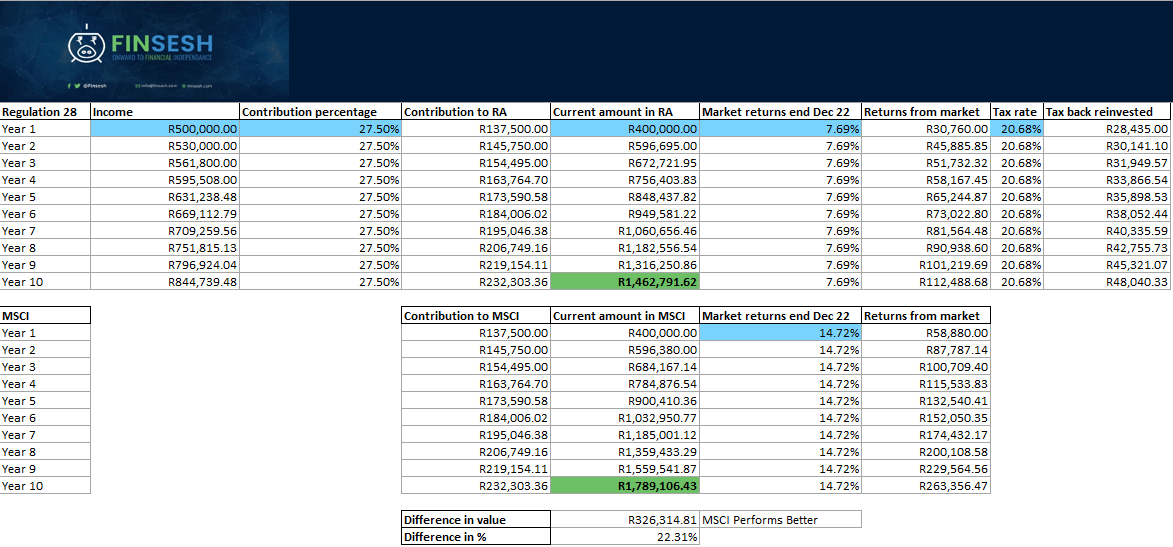

In the last 10 years ending 31 December 2022, the average regulation 28 fund (category average ASISA Multi-Asset High Equity) provided a return of 7.69% annually. The offshore investment we will use as a comparison is the MSCI World index. The MSCI World index invests in roughly 1500 large to mid-cap stocks of 23 developed markets globally. The proxy for the MSCI World index is the Sygnia Itrix MSCI World Index ETF which returned 14.72% annually.

In the snapshot below we used the following scenario: Person X earns an annual income of R500 000 and contributes 27.5% of the income to their retirement annuity each year. The current amount in their retirement annuity is R400 000 and their tax rate is 20.68% as calculated on their income with a tax calculator.

In the retirement annuity scenario, the second-year value is equal to the amount of the current value, plus the contributions for the year, plus market returns plus the tax refund being reinvested in the fund. This continues for 10 years.

In the offshore investing scenario, the second-year value equals the current value, plus the contributions for the year, plus market returns. No tax refunds apply here. This continues for 10 years.

At the end of 10 years, the retirement annuity value is R1,462,791.62 vs R1,789,106.43 in the MSCI world index fund. This is a staggering 22% more than the retirement annuity scenario. A big caveat is that no tax is taken into account on the offshore investing account, as we are assuming no withdrawals have been made yet. The idea is to illustrate that there are other alternatives out there.

Other factors influence the end portfolio value, such as current fund value, income level, market returns ect so we provided you with this comparison tool which is available here, for you to do your analysis.

Let's look at some of the factors at play below.

Retirement annuity factors

High contribution: Contributing 27.5% is a high margin for retirement savings. As you contribute less than 27.%, your tax rebate will start reducing as you are getting tax back on fewer contributions. This will impact your retirement annuity returns over time.

Not reinvesting your tax rebate: Let's be honest, receiving a tax rebate from SARS feels like free money. Notice in the scenario that the tax rebate in year 1 is close to the returns from the market in year 1. Not reinvesting your tax rebate will dramatically reduce your end portfolio value.

Access at retirement: Not only does this end portfolio value not stack up to its offshore alternative but your money is also locked in a retirement annuity fund until the age of 55. At retirement only of your money will be available as cash, the other must be invested in an annuity for income payments.

Regulation 28 offshore limit: In February 2022 the offshore limit increased from 30% to 45%. Which is a good thing. More flexibility of choice the better. Hopefully, in the future, this limit will be removed completely.

Prescribed assets and legislation changes: Prescribed assets are a law that prescribes pension funds to invest in certain government-approved assets. South Africa has a history of prescribed assets that was only scrapped in 1989. I don't want to invest in what our government thinks is a good investment if they can't even keep the lights on.

Emigration: With many factors in South Africa enticing people to look for greener pastures, they used their retirement annuity funds to fund the cost to emigrate. SARS changed the law on 1 March 2021, stating that only 3 years after you completed your emigration process and been a non-resident for tax purposes may you access your retirement annuity. This law will make it tough for many who saved in these savings vehicles to emigrate.

Offshore investing factors

The returns don't repeat themselves: A popular saying in the investment world is that past performance is not an indicator of future performance. This is very true. A risk you have is that the performance won't repeat itself and maybe be a little less than the last decade. Another risk is, what if it repeats itself and does even better? The question is if 23 developed nations' best companies will outperform South African companies, struggling with load shedding and other proudly South African problems.

Tax issues: Where retirement annuities have tax-free growth, the same does not apply to any discretionary offshore investment. Please consult with a financial planner to ensure you are in a tax-efficient tax structure that suits your tax scenario.

Unsure if a retirement annuity is for you?

If you're reading this you're looking for more guidance. Let's discuss a hybrid option, as this topic is certainly not black and white. The tax rebates can be used to invest in a tax-free savings account (TFSA) where there are no regulation 28 limits that apply. You can use your rebates to invest in offshore investments and form a hybrid strategy for yourself, getting the best of both worlds.

Your contributions to your retirement annuity can be split, where a portion will fund a TFSA up to its allowed maximum contribution. Ensure that you use your maximum TFSA allowance first and contribute the remaining to a retirement annuity.

If you still have not used any of your tax exemptions for discretionary investment such as the R40 000 per year exclusion on capital gains, or the R23 800 interest exemption. It will be wise to fund a discretionary investment account too as they don't have investment limits.

Summary

Retirement annuities are certainly not a one size fits all retirement solution. Weighing up all the risks and ensuring that our choice of investment suits your family's needs is crucial before making such a long-term investment. Don't blindly trust anyone with your money, take control of your finances and learn about your alternatives. At the end of the day, nobody cares about your money but you.

If you're still unsure, reach out on Twitter or send an email to info@finsesh.com as we will gladly talk you through your options as guidance, not advice.

If you want to find out more about becoming financially independent, please see our free course. If you want a blueprint toward financial independence, you can enroll in our Stages to financial independence course.

Onward to Financial Independence

If you found this blog post helpful please follow us on Facebook and Twitter @finsesh for more tips on Financial independence and sign-up free to stay up to date on your journey to financial independence with our personal finance money blog.

Related Tags:

Related Articles

All articles

July 26, 2024, 7:27 p.m.

Why do prices go up and down?

July 26, 2024, 12:05 p.m.

UNDERSTANDING INVESTMENT HOLDING COMPANIES

July 26, 2024, 12:05 p.m.

AUD/USD Market Outlook

July 26, 2024, 8:53 p.m.